💸 Mo Money, Mo Problems 💸

💥 We need your support to keep growing 🙏🏻 – know someone who would like to read these weekly updates? Forward this email to them or click the button below! 💥

To Operators,

Brrrrrrrrrrr. Globally, money printers haven’t let up since last March and there’s no sign of them stopping anytime soon, not with our boy JPow leading the pack anyway.

The macro environment has been deteriorating for years and COVID sped up the music. Currency issues started as a relatively harmless by-product of the 2008 Global Financial Crisis and have quickly become something more sinister waiting to surprise us all (except you dear readers you won’t be surprised).

The case for owning inflation-resistant hard assets, especially Bitcoin, has never been stronger with monetary supplies going vertical across the world.

Biggie put it best…

“Mo Money, Mo Problems” –Biggie Smalls

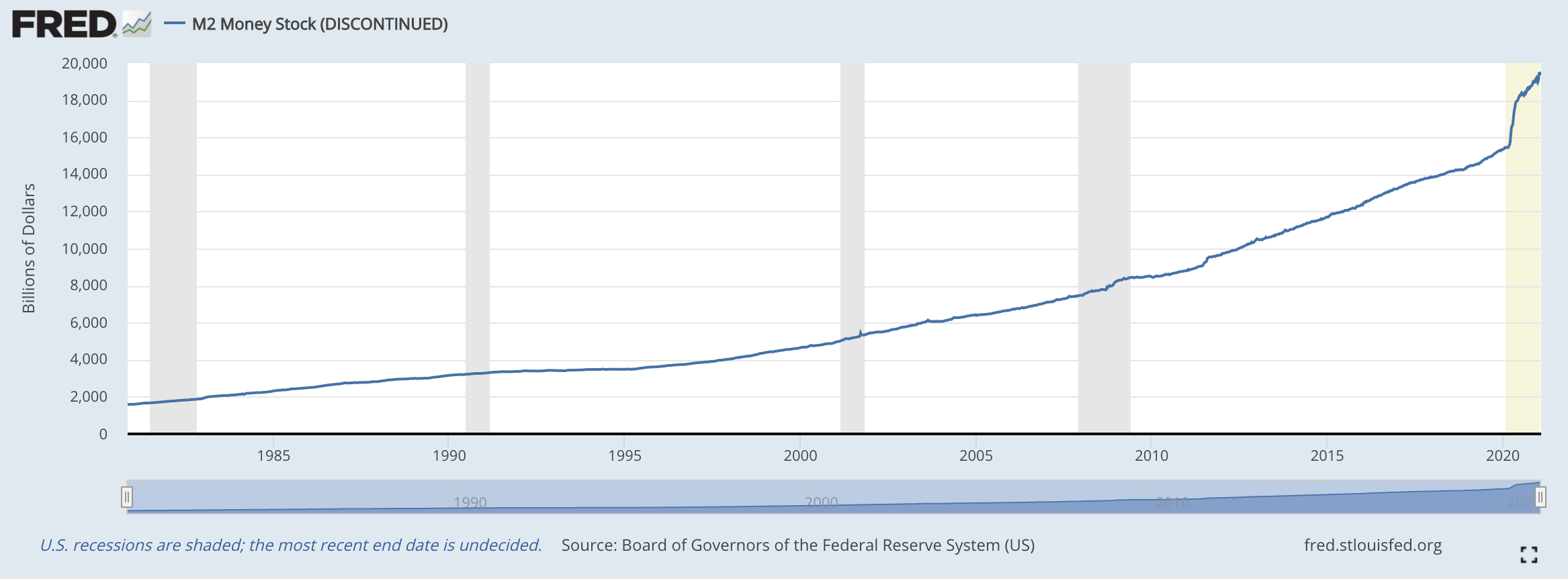

United States of chasing paper

From 1980 to 2010, the money stock of the US economy (M2 for you economists) grew at an annual rate of 5.7%. From 2010 to 2020 (pre-covid) it grew at an annual rate of 6.2%. From March, 2020 to today, M2 has grown 25.6%.

The cost of capital used to be about ~6% but now it is closer to ~25% — cash sitting in the bank is like an ice cube melting faster than ever before…

Before the COVID-era if you left your money in the bank you’d lose half your money in ~7 years due to inflation.

At the current rate this will take about 2 years.

All of this printing caused the prices of equities to explode upward as investor sought to keep up with the 25% benchmark.

This isn’t just happening in equities markets – real estate and commodities are seeing similar double-digit growth over the last 12 months.

Investors are fleeing cash for assets priced in dollars. Assets that they hope will appreciate at least as fast as the Fed can print money.

Annnnd it’s gone

The US government attacked COVID economically by leveraging Fiscal and Monetary Policy. Congress got money in the hands of people and businesses via the stimulus bills and the Fed propped up the economy by cutting rates to near 0% and injecting money into the monetary system via quantitative easing.

Largely it worked. Businesses got the support they needed and people deeply affected by the unemployment spike got assistance, but the problem is they never stopped or even had a plan for stopping the printing.

The current administration just passed it’s $1.9T stimulus bill and is currently working on another bill targeting $3T in infrastructure spending.

Meanwhile, the Fed has committed to near-zero rates for the foreseeable future and is continuing its quantitative easing (QE) programs.

Put bluntly, M2 is guaranteed to balloon over $20T and likely climb near $30T.

The ice is going to keep melting.

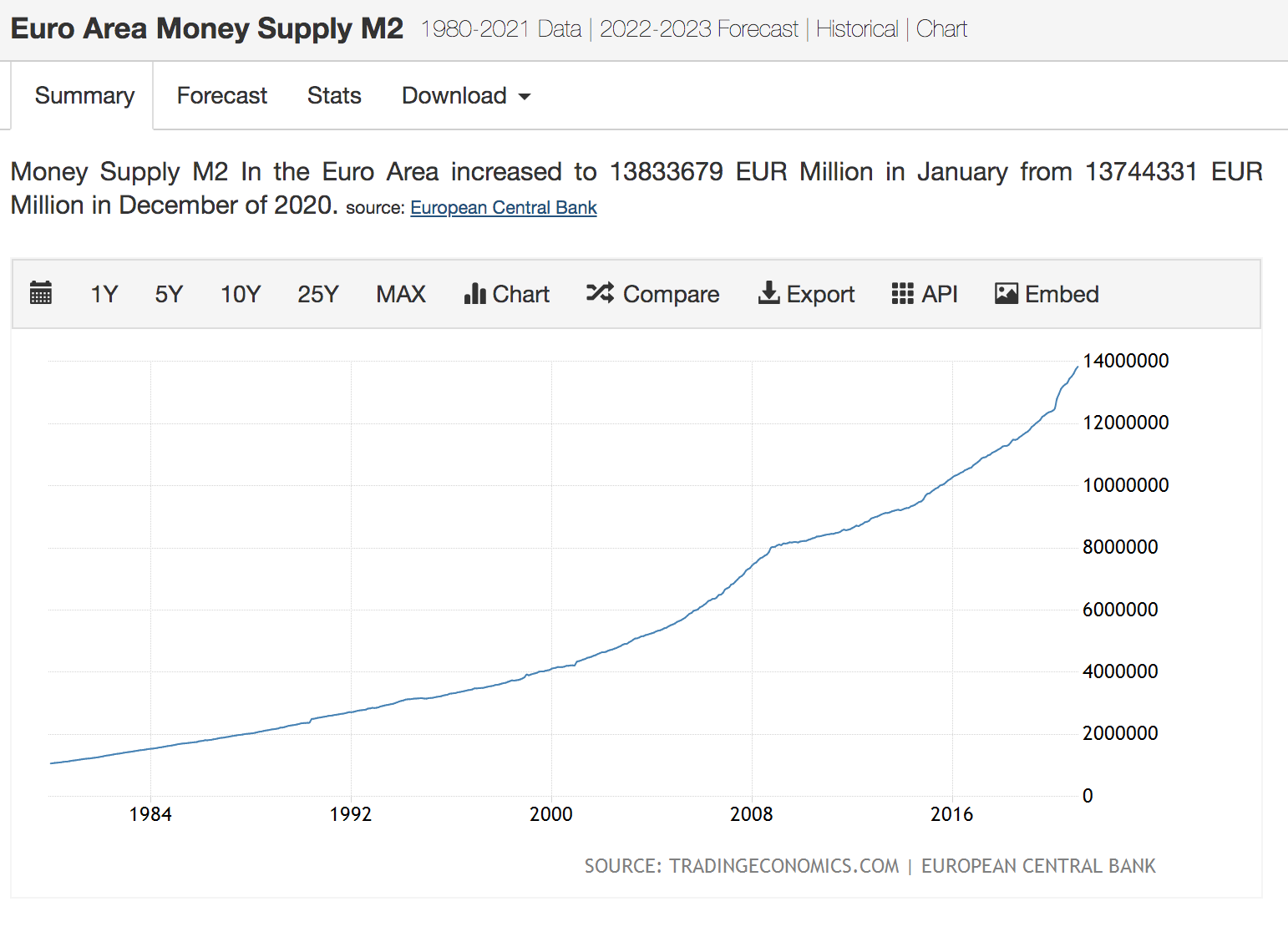

Across the pond

The US Dollar / Euro relationship is one of the linchpins of the global financial system and that means what’s going on with the Euro is important to watch.

The European Central Bank (ECB) has acted similarly to the Fed by leaning heavily on Monetary Policy to stem the effects of COVID. They’ve slashed rates to 0% and are continuing quantitative easing as well.

In fact, the trend of QE and near-zero rates is continuing across the developed world:

Note Japan has gone negative and the the only rates above 1% are in emerging markets.

Why haven’t we gone full Weimar Republic yet?

We know two facts:

Money stocks across the world are increasing at historical rates

The cost to borrow money is cheaper than ever

At the surface, this sounds like the perfect storm for rampant inflation, but so far we haven’t seen it yet. What gives?

Enter the Quantity Theory of Money. According to this economic theory, the price level of goods and services (PQ) is proportional to the money supply in an economy (MV).

When COVID struck we know 2 things happened:

Money changing hands, or velocity of money, plummeted – V ⬇️

Stimmy and QE happened – M ⬆️

The demand side (PQ) of the equation remained constant as price levels didn’t move and economic transactions were stagnant (both production and demand fell in-step).

Now a year into COVID and largely on the mend, we are faced with a growing problem: reopening.

People were largely holed up during the last year and didn’t spend much money. The personal savings rate has never been higher and America is sitting on excess cash.

You can start to see where this is going… what’s going to happen when businesses reopen? People are going to spend their money and in turn that’s going to drive velocity up.

Coupling a sudden increase in velocity with an already bloated monetary supply is a worse case scenario for prices (P).

With extreme pressures coming from the supply side of the equation, prices will have to yield to the impulse and move upward. When prices move upward quickly for a sustained period of time we get inflation. When prices do this very quickly we get hyperinflation.

Hyperinflation has infamously ravaged countries like South Africa, Venezuela, Zimbabwe and the Weimar Republic.

The effects are brutal and the pain is typically stopped by pegging the currency to another more stable currency or to a deflationary asset like gold.

Should the US enter hyperinflation our options are limited – we are the world reserve currency which rules out a currency-peg. The only option left is an asset peg and while gold is the obvious choice, Bitcoin can’t be ruled out as a contender.

The downsides to a gold or Bitcoin standard are complex and wide reaching but the key one to be aware of is that it takes away the US Government’s ability to print money at the drop of a hat — every dollar minted needs to be backed by some amount of asset.

This would mark a fundamental shift in how Monetary Policy has functioned since 1976.

Tl;dr

The stage is set. The Fed and Congress have bloated the monetary supply to historical levels while at the same time a global pandemic suppressed economic activity. As the world returns to normal, excess cash will begin changing hands and this will drive the prices of goods and services up.

Our best-case scenario is above-average inflation for the next few years and the worst case scenario is hyperinflation, with some kind of monetary restructuring on the other side.

The good news is that for hard assets like Bitcoin, gold, and real estate this is a perfect environment. Deflationary by nature, these assets will retain their value and appreciate significantly in dollar terms.

Equities will also do well but these are less hard given their supply characteristics. Additionally, debt is an honorable mention here as it is a solid play in an inflationary environment assuming you have the cash flow to cover payments.

Regardless of which way this thing goes, it’s hard to imagine that creating ~20% of all dollars ever in a year’s time doesn’t have consequences.

Forward and upward.

The Portfolio Rundown

The portfolio is down 11% against last week but flat against the week prior. The main story unfolding right now is in Bitcoin.

The orange coin is experiencing its 3rd pullback of 2021 and currently clocking in at -19% from local highs. Near term we’re likely not done seeing red as the near support is at the $47,000 level.

$BTC turning back upward prior to hitting to $47k is bullish, so is a bounce off that level. If it breaks $47k, expect a run towards $45k then $42k as traders look for lower support levels.

In terms of cycles and price levels, this looks to me like a typical pullback on the uptrend. As I discussed in my letter about cycles I won’t become bearish on Bitcoin until November or $100k, whichever comes first. This cycle is just getting started and there’s a lot of room to run.

Alts are falling in-step with Bitcoin but running a bit further. Cardano, Link, and Bancor have lost a lot of weight and make up the majority of my portfolio movement to the downside.

Silver-lining: Kleros has been moving inverse to the broader alt market recently and printed an 11% day when most alts and Bitcoin were red. Likely not a statistically significant event but cool to see anyway.

While these pullbacks are boring they do represent a great time to buy the dip #BTFD. If you’re looking for a sale on crypto you just got handed another one and I guarantee it won’t last.

✅ Thanks for reading Bitcoin Operator! Please ask your politicians, Federal Reserve Board Members, and friends to sign up.

Get $10 FREE automatically deposited to your account when you trade $100 worth of crypto at Gemini | Sign up today using this link HERE

Nothing in this email is intended to serve as financial advice. Do your own research.