💣The New Credit Default Swap💣

Bitcoin Operator writes for its subscribers and we need your support to keep growing – know someone who would like to read these weekly updates? Forward this email to them or click the button below!

To Operators,

Everyone knows the story of the Global Financial Crisis that occurred in 2008…

For those that don’t or maybe didn’t pay attention here’s a quick summary:

A housing boom that started in the early 2000s was quickly fueled by Wall Street into a multi-trillion dollar derivative monster. Mortgages (of ever decreasing quality) were being packaged into securities and sold across the financial world. Derivatives were built on top of these securities further expanding leverage on already questionable mortgages. In 2007, the bubble popped as Lehman Brothers succumbed to their own leverage (32:1) on derivatives triggering the recession that would follow.

But what a lot of people don’t realize was that buried in the carcass of the 2008 GFC was a story that would come back around just over a decade later: The Birth of the Credit Default Swap.

A credit default swap (CDS) is a financial derivative or contract that allows an investor to "swap" or offset his or her credit risk with that of another investor.

Credit default swaps were nothing new in the 2000s, they had been around since 1997, but they were obscure derivatives used to offset risk in creative ways – not mainstream financial products.

CDSs really came into their own when a few savvy investors began to use them to effectively create a short position against the housing market via mortgage-backed-securities (MBS).

If you’ve seen the movie The Big Short then you remember the scenes where Dr. Michael Burry was laughed at when he approached major banks to buy CDSs – the banks thought it was laughable Burry intended to short the housing market, an industry that was traditionally the bedrock of America, but took his fees and carried on.

![The Big Short (2015) - Dr. Michael Burry Betting Against the Housing Market [HD 1080p] animated gif](https://substackcdn.com/image/fetch/$s_!CONN!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fbucketeer-e05bbc84-baa3-437e-9518-adb32be77984.s3.amazonaws.com%2Fpublic%2Fimages%2F9f954d96-005a-473b-8d28-a304c8139697_1280x534.gif "The Big Short (2015) - Dr. Michael Burry Betting Against the Housing Market [HD 1080p] animated gif")

Burry was laughed at not because he was wrong but because he was early. By 2007 the market for Credit Default Swaps had gone from less than $1T to a $62T market:

In just a few years swaps went from an obscure derivative to somewhat of a consensus trade. Banks had re-tooled and were selling the sh*t out these things to anyone who would buy, and buy they did. Instead of booking bespoke meetings like Burry did, swap buyers could simply call up dedicated trading desks at any major bank and get exposure – the plumbing had been created because there was demand.

This story doesn’t have a happy ending. Burry ended up walking away with hundreds of millions of dollars but lost his fund in the process and the US economy ended up in the worst recession seen since the Great Depression…

So what does any of this have to do with Bitcoin?

The morale of the story is this – despite the consequences (intended or not) Wall Street never passes up on a chance to make money. Full stop.

And Bitcoin isn’t any different.

For part 2 of this saga we have to tell the story of a guy named Michael Saylor and his technology company, MicroStrategy.

Credit Default Swaps 2.0

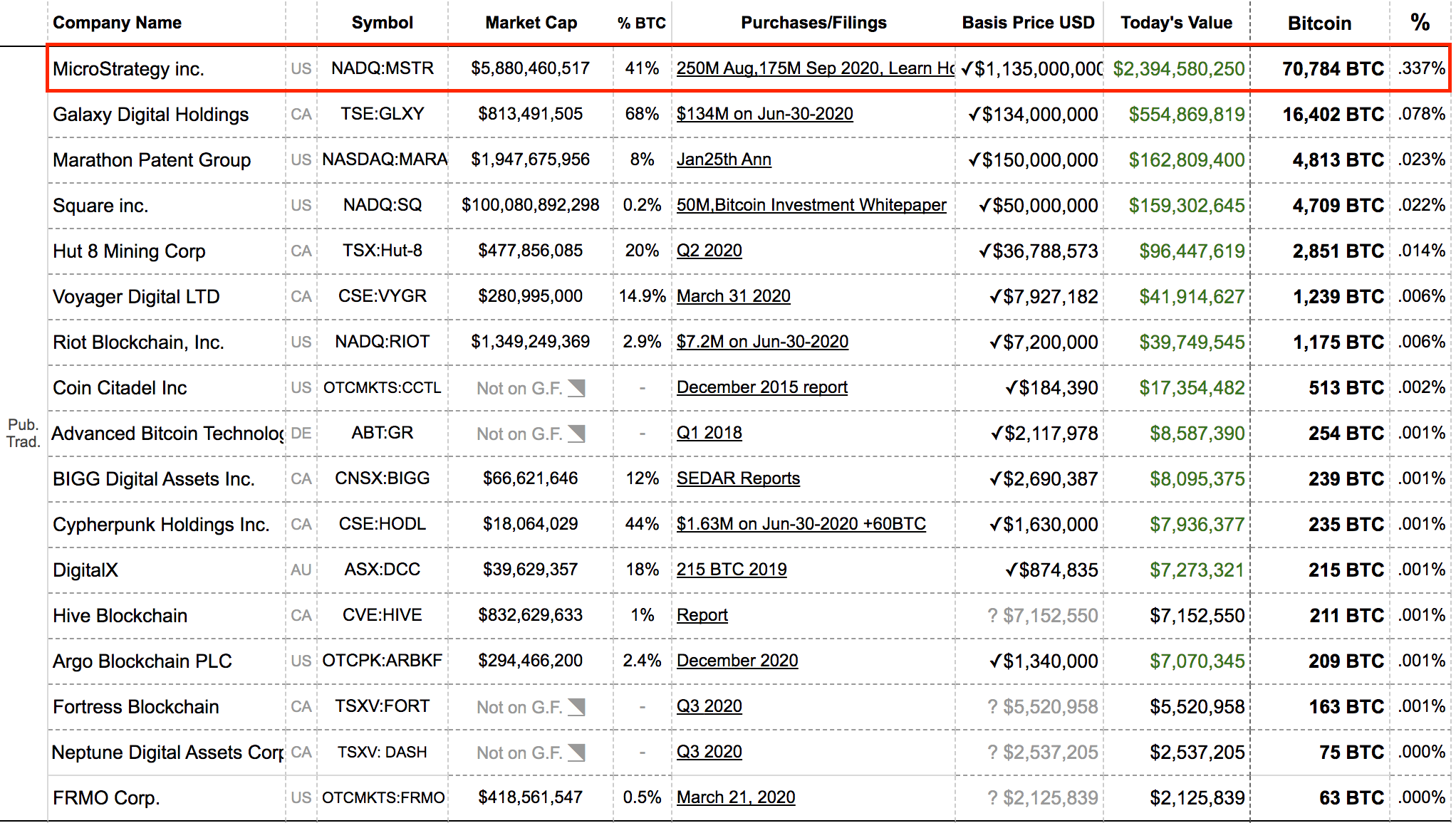

As of today, 17 publicly traded companies hold Bitcoin on their balance sheets but only one does not conduct business operations directly related to crypto.

In 2020, at the direction of the companies CEO, Michael Saylor, MicroStrategy purchased 70,784 bitcoins in accordance with their treasury reserve policy (below).

While this purchase is huge news for Bitcoin – the bigger news is how the buying was done. Saylor purchased the company’s bitcoins in two distinct transactions:

MicroStrategy purchased bitcoins using cash sitting on the company’s balance sheet in accordance with its treasury reserve policy

MicroStrategy issued a convertible bond with the sole purpose of buying BTC

#1 is mildly interesting – there are tons of public tech companies sitting on piles of cash that could convert some percentage to Bitcoin, but this is likely a tough sell to investors and certainly creates a PR challenge for the company.

#2 is where our two stories come together. The convertible bond issuance was created with the sole intention of buying Bitcoin. Investors didn’t need to be convinced because they knew exactly what they were buying.

The bond was oversubscribed.

Originally targeted at $550M the bond closed at $650M. Since all of this buying, MicroStrategy has gone parabolic:

The Bitcoin play was Michael’s genius but the market’s reactions is telling – public market investors are drooling for Bitcoin.

By mandate, most institutional public markets players are barred from investing directly into Bitcoin but have free reign to pursue equities or debt instruments. A debt instrument created by a company on the Nasdaq is the perfect vehicle for institutional allocators to get Bitcoin exposure without running afoul of their own rules.

There exists extreme demand for Bitcoin in public markets and now there also exists a proven instrument to introduce supply.

The only thing left to do is make a market – banks are already on board, you just need willing companies.

Saylor’s bond is like the first credit default swap ever issued. At first he was laughed at but now people are starting to come around…

In an effort to spread the good word of Bitcoin, Saylor has written a Bitcoin-for-public-companies playbook and is sharing his knowledge through hosted events. The interest has been massive and people are curious.

Tl;dr

Public company issued convertible Bitcoin bonds are the new credit default swaps.

Like everything in crypto, timescales are compressed. Q4 2020 was akin to 2004 when Dr. Burry started buying his first credit default swaps. Q1 2021 is starting to look like 2005-2006 where the swap market was gaining interest and starting to grow.

In the back half of 2021 I expect to see significant growth in the number of public companies holding Bitcoin – likely purchased through a convertible bond.

Catalyzing this will be two things:

Increase in Bitcoin hype and awareness

Inflationary pressures

The media and crypto-heads like Saylor will take care of #1. I believe #2 already exists and people believe it, but we’ll need to see action around these beliefs.

i.e. the investing public and company leadership needs to make the jump from “30% of all USD created was printed in 2020 yea that sounds bad” to “wow the Fed is printing the Dollar into oblivion, I better do something about this”.

Bitcoin can be boiled down to classic supply and demand dynamics. With supply fixed, price becomes a demand-side equation. Public companies dropping billions of dollars into Bitcoin in aggregate is net-positive for demand on an already existing supply shortage. The Bitcoin Bond™ (not actually trademarked) will certainly not be a one-off case study with MicroStrategy.

Forward and upward.

The Portfolio Rundown

Bitcoin continues trading sideways in the $35k range. While this may be boring in the near term it’s providing two things:

Consolidation around $30k support – the days of $20k Bitcoin are likely history

An opportunity to accumulate

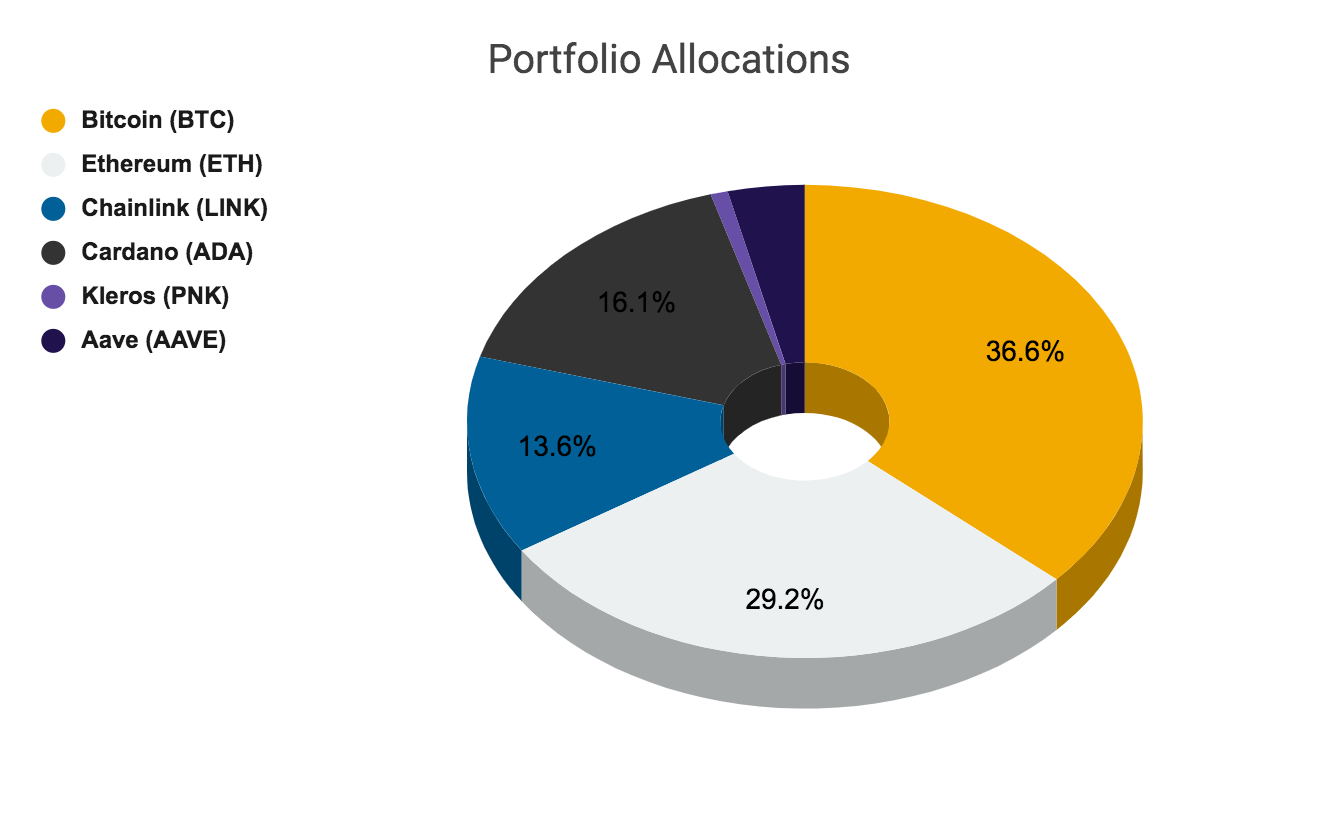

Throughout this period I’ve been adding to many of my positions and have seen some great results in Cardano, Chainlink, and Aave.

Like Bitcoin, Ethereum has also been consolidating. It looks to be gathering strength around $1,300 and priming for a move upward. This bull flag (note falling volume) is a classic set up and I’m excited to see what comes next:

At the macro level, recent action in meme-stocks like $GME and $AMC has likely driven liquidity away from crypto as retail investors pour money into these equities. While I don’t think those sagas are over (#holdtheline) I do think the manipulation and inside baseball being played on retail is going to push a lot of people towards crypto – a place where financial incumbents hold little to no power.

I’ll be watching these stories this closely over the next few weeks.

Get $10 FREE automatically deposited to your account when you trade $100 worth of crypto at Gemini | Sign up today using this link HERE

Nothing in this email is intended to serve as financial advice. Do your own research.